Class 3 Valuation: Groundwork for intrinsic valuation

Be aware of weapons of Mass Distractions - with words like "control", "synergy" & "strategic".

By this class, you should have a company in mind that you want to value now to practice. This company can still be changed later.

↓↓ Make sure you read Class 2 first:

Knowing how to “DCF” can impress people but a lot of DCFs don’t pass the smell test, especially DCFs from investment banks due to mismatching & inconsistencies.

Discounting needs to be consistent.

If you look at a business, you can either value the business, or value the equity of the business. Easiest way to separate business & equity, is to think of buying a house.

Unless you’re a drug dealer, you’ll have to borrow money to buy a house. You take a $1.6 million loan to buy a $2 million house. The difference between the 2 numbers, i.e. $400,000, is your equity.

6 months later, the house price is down by $400,000 & it is now worth $1.6 million. Your equity is now worth nothing. The bank now owns 100% of your house.

You can value businesses where equity is nothing because you borrowed so much, the value of the debt is worth more than your business.

You have a choice, to value the business (house) or to value the equity.

Cash flow to equity holder means free cash after debt repayments (principals & interests). The discount rate applied in DCF will be the rate of return as an equity investor (cost of equity).

Business can be funded by 2 capital providers, equity shareholders & debt lenders. As equity investors, cash flow to you will be either in dividends or residual cash after all payments made (which may not be dividend out but retained). Cash flow to debt lenders will then be just interest & principal payments.

These 2 collective cash flows produce for both capital providers are called Cash Flow to Firm. If this cash flow is what you are discounting, then the cost of capital has to be a weighted average cost of both debt & equity providers (i.e., Weighted Cost of Capital, WACC or Cost of Capital as prof simplifies it). This gives you the value of the entire business.

You then subtract the debt outstanding and any other contingent liabilities to get equity value.

Hence, first principle in valuation is not to mix discount rates on type of cash flows.

A Case Study on First Boston’s M&A advisory deal for Kennecott

In the 1970s, there was a coal mining company called Kennecott where they received antitrust instruction to divest 1 of their subsidiaries. Through this divestment, they received $600 million in cash.

Instead of returning back the cash to shareholders (first mistake), they went to an investment bank (second mistake) to look for acquisition target (third mistake), which was then overpaid for (fourth mistake).

Target company was Carborandum Co. (alt. source 1, alt. source 2), an abrasive producer based in Niagara was suggested by the investment bank, First Boston precisely at the price of $600 million, justified by a valuation by the investment bank & due diligence done, which was 2x of the Carborundum’s book value.

The investment bank uses the Carborandum cash flow to equity (FCFE) to project the valuation. Which of the following discount rate should be used?

By elimination, cost of capital (WACC) should be discarded since FCFE was used.

If Cost of Equity (Ke) is the choice, whose company Ke should be used? The acquirer, the target or the merged entity?

Since the acquirer is forking out the money, should it be then the acquirer’s cost of equity? No.

The cost of equity should be based on the target, the project, or the subject. Otherwise, if you are a stable firm with low cost of equity, all high-risk investments will be very attractive. This was the mistake of AT&T in the 90s, a telco company that went to acquire all high-risk tech companies.

They don’t look cheap; it was just wrong discount rate applied.

Don’t even average the different discount rates! If 1 person is overweight & the other is underweight, average them doesn’t make sense. Both won’t even-weight!

So, 16.50% (Target’s Ke) is the correct cost of equity to use.

What’s the worst number First Boston can use?

10.50%, Ke of the Acquirer. Is 1 thing to lower a discount rate to inflate valuation, but it’s cardinal sin if you use the wrong discount rate to begin with.

By changing to the correct Ke of 16.50%, the valuation of the target company is now only worth $400 million, Kennecott was $200 million overpaying for Carborandum.

The 2 leaders in First Boston M&A team were Bruce Wasserstein & Joseph Perella whom later formed Wasserstein Perella & Co which was mentioned in Class 2 of Valuation where Prof. said they can’t value anything.

Consistency also applies to currency as will be taught in later class.

The essence of Intrinsic Value

Nothing grand about Intrinsic Valuation, is just based on fundamental assessment of expected cash flows generated by an asset and the uncertainty of this cash flow.

Most of the DCF architecture was developed by John Williams in 1937 (before Ben Graham!). Intrinsic valuation pre-dates DCF. You don’t need to know DCF to do intrinsic valuation, it is just a way of thinking to know how much to pay for an asset.

Certainty equivalent of cash flows - how certain are you on the expected cash flows?

There are only 2 answers - uncertain, which would be reflected in by discounted with a risk-adjusted discounted rate or very certain, which would be reflected in by discounted with a risk-free rate.

Best is shown in a game show example as Prof. uses - Let’s Make a Deal by Howie Mandell.

Howie Mandell presents you with 2 suitcases, 1 is with a million bucks & the other is nothing inside. Howie Mandell will offer a sum of money for you to walk off from a deal. The expected return of this deal is $500k but people who played the game, will walk off with $400k or $300k because the certainty of equivalent cash is there.

If you value Coca-cola with $1 billion of expected cash flow for the next 10-years then a Howie Mandell comes in & says the guaranteed cash flow is $0.8 billion. You would replace the cash flow of $1 billion to $0.8 billion (certainty equivalent), but you will then discount the cash flow with a risk-free rate.

A famous quote from Warren Buffett is that he doesn’t adjust his discount rate but just used a risk-free rate. This stems from the fact that he likes & uses “certainty of earnings”, by looking at businesses that is easy to forecast.

You can do a Warren Buffett style of ascertaining a very certain cashflow, but don’t double count by using a risk-adjusted discount rate. If certainty of cash flow is there, use risk-free rate.

However, unless you are Warren Buffett, it is very hard to do a “certainty equivalent cash flow”. Hence, use a risk-adjusted discount rate on your best guess estimated cash flows.

The real game of Intrinsic Value using a $20 envelope

Imagine Prof is selling you an envelope with $20 in it, how much would you pay for it?

In a bidding scenario, the final price will stop at $20.

If the envelope has the word “Control”. How much would you pay for it now? You now have $20 + “Control”. How much is the envelope worth now?

When you do M&A valuation, why would you add a 20% premium when there’s control given while the cash flow doesn’t change? Try buying the envelope for $25.

How about putting the following on the envelope - synergies, brand name, ESG, sustainability? These are weapons of mass distractions as prof. calls it.

Those words don't change a valuation. Somehow these keywords are always brought up once a valuation is done, not before.

There are also 2 words that have worked consistently for the past years - “Strategic” & “China” as a source of premium.

Strategic deal = a really stupid deal that you don’t want to do but will do it anyway. Want to sell a business? Find a strategic buyer. They already made up their mind to want to buy your company before even due diligence or negotiation started!

3 years ago, “China” was the source of extra zeros. Today, it is reversed.

Following are rules to make sure you don’t fall for the trap of mass distraction:

If X doesn’t affect cashflow or risk of cash flow, then ignore X. Quantify the X into earnings & cash flows, not a plug number. Brand name = pricing power, hence, adjust cash flow to reflect the higher margin. Show X in numbers. Synergy is not 2+2=5, it means each of the company couldn’t do something before separately but once merged, will be able to do those things, quantify those things.

Uncertainty is a feature in valuation, not a bug. Don’t fall on the trap of “I don’t invest in things I don’t understand”, the older you get, the more things you won’t understand. Is the nature of getting old. Sometimes, you don’t know as much but you still need to try to estimate. Otherwise, you’ll be valuing Coke all your life.

Expected negative cash flows means no value. For an asset to have a value, it has to have positive cash flow sometime in the future. Stupid business & stupid capital providers exist but doesn’t mean the business should have a value. If is negative expected cashflows forever. No need DCF to know valuation is negative! MoviePass was a failed startup that allows you to watch unlimited cinema movies for only $9.99/mth. The CEO mentioned that the average American goes to 1 movie a month. You can drown in a lake with an average depth of only 6 inches. Self-selection exists in deals like this, it will attract bargain hunters which will bankrupt the company. What once a month will become 20 times per month because of free.

Positive cash flow in later years would usually means high growth & high cash flow in later years. This is common in young companies with negative cash flow in first few years where it will explode up once cash burn is over. Hence, is normal to expect very high cash flow growth once breakeven or critical mass is achieved.

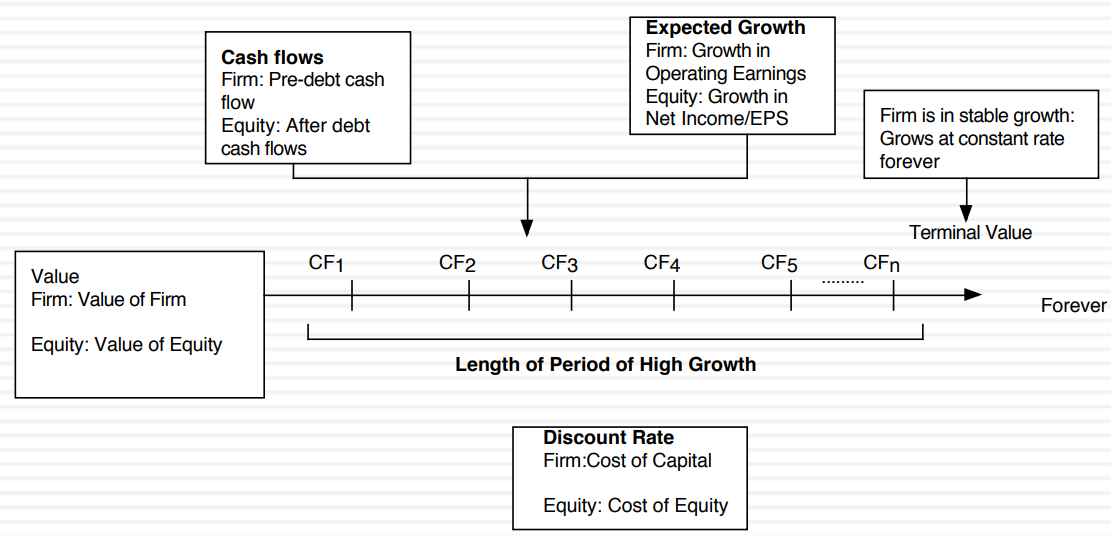

How to get Equity Valuation (it gets technical)

First, is what debt to subtract from FCFF to get FCFE?

Value of long-term debt

Value of all debt

Only debt that are used in cost of capital calculation

All liabilities

Leases

Contingent liabilities like lawsuits

We'll get back to this.

Take a look at the following cash flows & valuations, both methods of using FCFE or FCFF would give the same equity valuation. This is where valuation is done right.

The generic DCF

The generic DCF is a matter of discounting expected cash flow with risk adjusted discount rate.

Expected cash flows can be forever, because of the assumption that companies can last forever. This is where Terminal Value comes in to put a stop in forever cash flow. Terminal Value begins when you assume your cash flow grow at a constant rate, forever.

Where do you start Terminal Value? Where a company hits the Growth Wall, where there is no more high growth but at a growth rate that is either same or lower than the economy’s growth rate.

(8x EBITDA at terminal year, is not Terminal Value, use the constant rate growth formula instead)

Every company will hit a growth wall best example is Walmart or maybe even Tesla now where it is profitable now. They become a matured company at this point.

Dividends vs FCFE

Dividends are easiest equity cash flow to estimate (net income x payout ratio) and put a valuation on. However, not all companies pay dividend, even those who can afford to with big cash pile (most tech companies). Once you pay dividend, it is almost becoming a policy where you have to stick to it. Hence, it is easier to just buyback shares.

FCFE is the next best equity cash flow where all residual cash flow is assumed to be dividend out (though not).

The discount rate for dividend or FCFE, whether at expected cash flows or terminal value is Cost of Equity.

WACC is use on FCFF (pre-debt cash flow).

Using Adani Group as an example on the pre-DCF process

First, is to look at the company’s past & understand the business. Adani is an Infrastructure business that has grown 10-fold over the past 10 years with very thin margin & high gearing.

…When you are forecasting, you are going to feel nervous. So is everyone else. You can only estimate what you can, don’t forecast the unforecastable, i.e. a black swan or any discrete uncertainty.

…You start with the top line revenue because margin changes throughout. Unless margins are already fixed, you can go direct to NOPLAT (Net Operating Profit Less Adjusted Tax) like most investment bankers do as a starting point.

…However, for a business that is in transition to a different business model, then historical numbers won’t be useful in forecasting. For e.g., Netflix from DVD business to streaming.

Read prof’s blog post on Adani to understand more about this process as he explained in detail.

The D in DCF

While we should now know to use the relevant discount rate for FCFF or FCFE. There is also appropriate discount rates for currency & nominal/real rate.

A US currency cash flow should be discounted with a US discount rate, a EU currency cash flow should be discounted with a EU region discount rate.

Similar, if the cash flow is already reflective of inflation, so should the discount rate, i.e. the nominal rate.

Discount rate should reflect the risk perceived by the marginal investor in the company.

Risk Adjusted Cost of Equity = risk free rate in the country of analysis + relative risk of company x Equity Risk Premium required for average risk equity

Understanding Uncertainty

Economic vs estimation uncertainty - Economic uncertainty is always there as economy is dynamic & changes, more data doesn’t mean more accurate. You do everything you can on economic uncertainty, but you should stop at one point & focus more on estimation uncertainty as it can be fixed with more data collection.

Micro vs Macro uncertainty - Micro deals with company specific uncertainty (e.g. management, products & business models etc). Macro deals with ecosystem uncertainty (e.g. regulations, environment, etc). Discount rate reflects only macro uncertainty.

Discrete vs continuous uncertainty - USDEUR currency pair is a continuous uncertainty faces a US business that has exposure in EUR. Same with interest rate risk changes. Discrete uncertainty happens suddenly, like the shorting of Adani Group or a failure of FDA approval.

// Class 3 of Valuation ends