Class 16 Valuation: Tying Up Intrinsic Value

From finance opaqueness to oil price tantrums - how to value Volatility, Uncertainty, Complexity and Ambiguity.

Today we’ll wrap up intrinsic valuation before going into pricing & multiples in next classes.

Recapping from the ending session of last class, banks’ financials are opaque as you don’t know what’s behind the numbers. You accept this opaqueness because you trust the regulators to do their job.

It’s accepted now that we can no longer trust the regulators post-GFC. We as in collectively the investors & the depositors. Not just post-GFC but also more evidently in 2023 of recent year due to the fall of SVB & Credit Suisse’s $3B residual value sale to UBS.

Due to this, you can no longer use the old way of Dividend Discount Model (DDM) in valuing a bank. If you use DDM, it means you are trusting the bank to act sensibly in managing risks, or trusting regulators in doing their job of regulating. Thus, having the dividends to be paid out perpetually. A tall order!

In 2009, prof. re-think on how he could value a bank. As cash flow is paramount in “DCF”, he ran into a brick wall. The traditional formula of using elements like changes in working capital, capex or depreciation in estimating free cash flow do not work for bank, or any financial services firm.

Then prof asked, “For a bank to grow, what does it need to re-invest in?”

1 peculiarity is that bank has to bring in equity as reserves due to regulation’s requirements. The more (loans) you grow, the more equity you need.

Losses & fines will also causes this equity (Tier 1 Capital) to increase.

Hence, the key driver for growth in a bank is about this “required reserved capital”.

The formula for FCFF becomes “Net Income (-) additional required reserve”.

A growing bank therefore will have less “cash flow” to pay out as dividend as it needs to lock more reserves in as equity.

Prof uses Deutsche Bank (←wiki links point to a list of controversies) as an example for such model & reference it being like a horror movie character, that you thought the monster have died but it reappears again, die again & reappears again.

His blog post in 2016 - A Greek Tragedy at a German Institution is worth the read to understand more on how German’s precision failed like a Greek pariah due to 2008’s GFC. All banks are hurt by GFC, but Deutsche, like the horror movie, keep getting hurt by it every year since then (but still doesn’t die).

For context, below is a chart comparing DB’s performance (dark blue right at the bottom) since peak of pre-GFC to now July 2024 agaisnt some notable mega banks. Goldman Sachs (pink) & Bank of America (green) emerged stronger while DB & Citigroup (light blue) remains dead in the basement.

Due to the constant losses in DB post GFC, the required equity injection or Tier 1 Capital becomes larger. DB is now severely underfunded & with rumour of being bailed out back in 2016. (Can’t really go bankrupt due to depositors money that is insured by the central bank usually)

Tier 1 Capital Ratio for Money Center Banks are generally higher because of larger dealings with governments, inter-banks & large corporations.

Prof computed that the average T1 capital for this group of banks are 15.67% but DB only has 12.41%. As part of modelling, prof increases this ratio yearly to reach 15.67% at the terminal (Referencing the 2nd row of the table above).

At first glance even before modelling, it does looks like there’s no hope as the bank is money losing, needs severe equity injection & at risk of a bail out (that could wipe out shareholder’s value). However, it is still 1 of the largest bank in Europe (ahem, remember Credit Suisse?) and we model it with a path for 10 years that it can return back to positive cash flow & with ROE that is the same as the Cost of Equity (no excess return). Not overly bullish but since valuing it means with some positive bias of going concern as previously learned.

You’ll see that ROE starts negative, which steadily increases to match Cost of Equity at terminal, showing improvement in business.

“Investment in Regulatory Capital” is what is needed to bring such improvement. Realistically, this is in the form of raising fresh equity, which would bring into a bank run due to this negative signaling effect.

“Cost of Equity” starts high using samples from high-risk banks & it tapers down as business stabilises with FCF improvement.

With SVB, what new things prof has discovered?

Duration mismatch of “borrow short & lending long”- can be reflected in a higher Cost of Equity as you are always 1 interest rate hike away from catastrophic failure.

The calculated value of DB was $20.67 while the shares was traded half of it. Like any valuation of real-life distress company, did prof bought DB shares? He did & it wasn’t a good buy.

Lucky for him, DB did a Rights Issue to raise fund, this allows shareholders to trade away that right to subscribe if they chose not to invest further. Prof didn’t want to invest further and thus cashed out 2/3 of his investment via this route & remaining is left holding still until today (as of 2023).

Fintech

As a closing to this section, not all financial services are valued the same. Master/Visa are payment processors. An Indian version of this is PayTM, which was invested by both Softbank & Warren Buffett, what a strange combo!

How payment processors earned is via a Take Rate, normally 2%- 4% of transaction value. Amex is at 4% hence not many merchants carry them (It’s a rich man’s card, to get high spending customers, merchants are willing to pay this premium).

PayTM’s take rate was 0.7%, way low than benchmarks but with TAM of 300 million users in India. Like any fintech, this was a way to acquire users & encourage adoption.

In Valuation, you need Free Cash Flow, which is derived from profitability. To increase in value means to increase profitability.

Hence, prof. assumes that PayTM will come to its senses of increasing its take-rate to 2%.

Prof’s big story on this valuation is about how to monetise big mobile users base of India. The value obtained was INR2,190/share. The IPO share price was around INR2,800. Today is at ~INR461 (down 80%), without any profit still (despite the bull market)!

Prof got it wrong & the biggest assumption wasn’t about the market sizing, but about wrongly assumes the management knows how to run business! They are busy in giving away freebies & signing up users even when the user count is already at 300m+. With such big userbase & depressed valuation, is it ripe for acquisition by foreign players like M/V or A? Only if it can turn profitable first!

Intangible Assets

A quip about accountants again, why create such separation of tangible and intangible. Cash flow is derived from assets, doesn’t matter if it’s tangible or intangible. Problems created by this accounting rules are:

R&D becomes an opex (that is not separated out in SG&A) rather than as a capex (that is separated out in Cash Flow from Investment) to clearly find out reinvestment amount.

Operating margin & hence return on investment can’t be calculated outright accurately to ensure you are re-investing right agaisnt cost of capital.

The above affects all tech & pharma companies and usually a lot of adjustments are made to find out the true margins, reinvestment rate & ROIC.

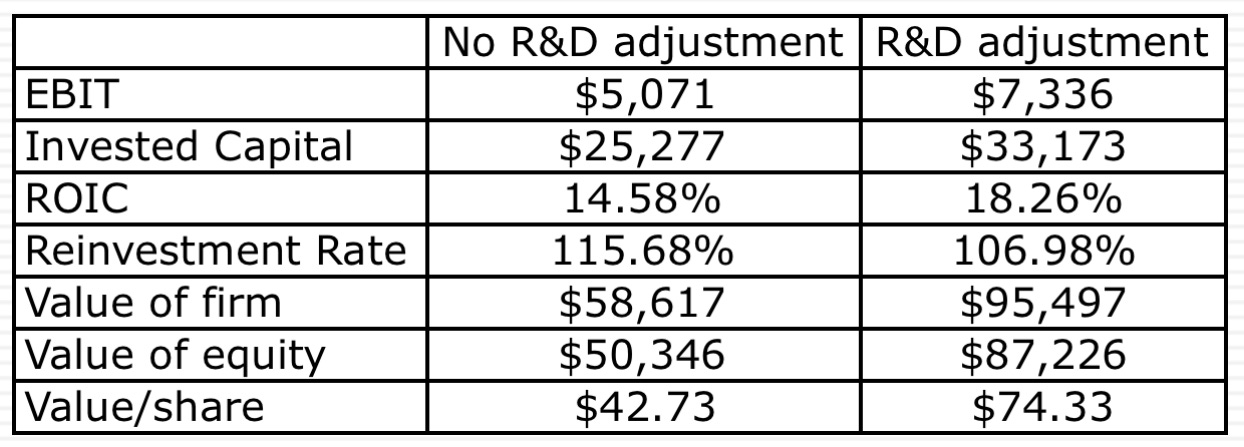

Using Amgen’s financial as an example to illustrate where R&D is being stripped out from P&L.

It shows how understated valuation is if no adjustment is being made, from $50m to $87m equity value, almost doubled.

Your view on these companies suddenly change. This is why most profitable tech stocks are actually not expensive (with share price growing) after adjusting for such intangibles (R&D or even certain % of staff costs that are due to software engineering or product developments)

Cyclical & Commodity Companies

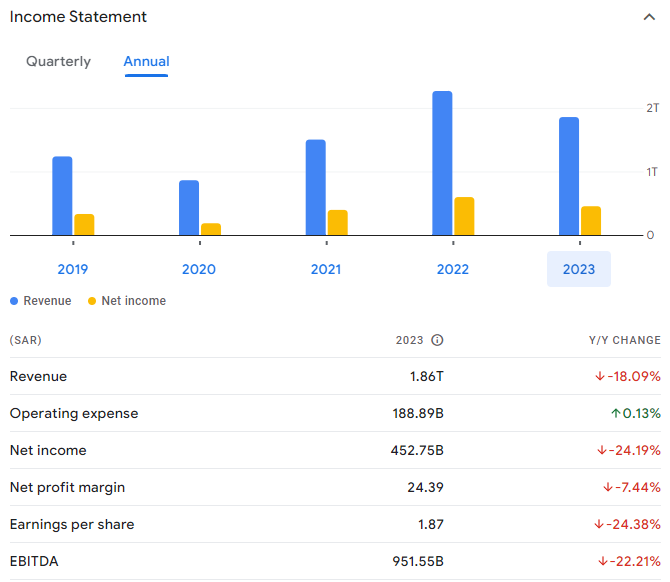

Taking a look at Aramco, a mature oil company and yet it’s operating income fluctuates like yoyo:

Doesn’t behave like a mature company at all. That’s because it is driven by oil price, or by macro effects.

Companies like these swings from being a bad company, to a good company very quickly.

Do you then forecast oil prices? i.e. it grows 10% p.a. next 5 years? If this is the method, oil companies will sure looks cheap today. There’s no need to value.

If you are really good at forecasting oil prices, go trade oil futures instead of looking into energy companies!

We need to separate the 2 components. What we think about the company (micro), and what we think about the economy (macro).

In fact, try to be macro-neutral. Use oil price as it is today (not even expert views that you spent $1000/call on) & value it with growth assumptions based on long-term historical.

Below is a valuation sample on Shell as prof did in 2016.

The question to ask is NOT what value will Shell be if oil price rises by 10%. BUT what is the value of Shell today if oil price is at today’s price.

There’s still 1 problem. The base year of your DCF still has the effect of oil price if you are using the last 12 months revenue. If is a bull year, this base year itself will be overestimated, which will in return over-estimate future revenues.

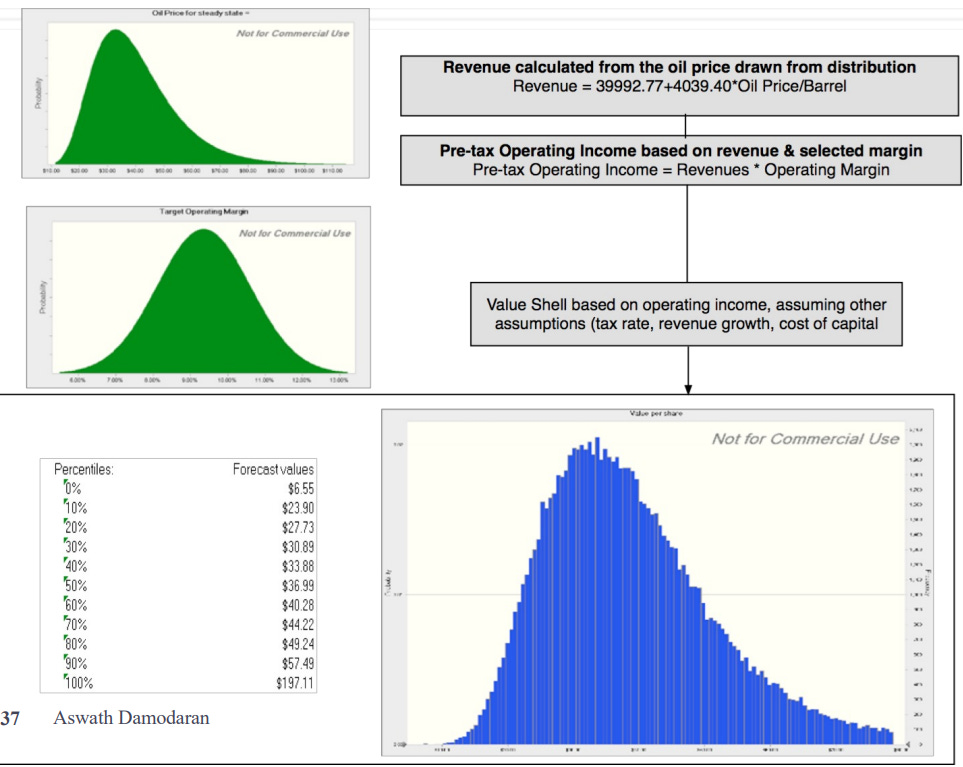

Hence, prof tried to even extract out how much of oil price is affecting revenue via correlation analysis.

The coefficient point of $4,039m, the slope of the correlation analysis means that for every $1 increase in oil price, Shell’s revenue is raise by $4b.

Prof then pluck the current oil price of $40 into this correlation formula to derive a predicted base revenue of $201 billion and starts to project from there, resulting a value $39.31.

The above value is still theoretical, as it doesn’t reflect the real world possibility that oil price will go up or down, in which will affects the valuation.

This is where Monte Carlo simulation comes in. Using the same regression formula, at least 10k data points of oil prices are imputed through the simulation of running the model.

Below is the distribution that was generated. At the mean, it doesn’t run away from the derived value. So it’s pointless? No, this way it at least give a more educated perspective on what exactly the value is should oil price lands on any of this distribution percentile.

// end of Class 16 Valuation